There are many ways you can find the best home-insurance deal. You can shop around to get the lowest rates. The companies that come recommended by others will be cheaper, but you must be careful not to compromise on quality or coverage. The insurance premium is how much you pay each month if you do not make any claims. Another consideration is the insurance deductible. This refers to the amount you will have to pay from your own pocket before your policy covers something.

Higher deductibles

Higher deductibles may be possible for homeowners with low or moderate incomes. This could lower your home-insurance costs. A higher deductible means that you will have to pay more out of pocket. It is worth taking the time to calculate your monthly expenses. Make sure to consider how much money you have saved for an emergency fund.

Apart from paying the deductible amount you must also select the type of deductible. There are two types basic deductibles. One is the percentage deductible, and one is the fixed dollar deductible. Fixed dollar amount and percentage deductibles let you choose the exact amount upfront. Percentage deductibles are determined by the home's worth. You can also choose a split deductible, which allows you to have part of your coverage under a dollar amount deductible and some under a percentage deductible.

Coverage limit lower

You can lower your home insurance coverage by asking a few questions. First, your insurance provider sets the dwelling coverage limit. It is based off the Replacement Cost Estimate of your home. You can verify your property details by contacting reputable homebuilders in your region to determine if this limit is appropriate. After you have determined the correct limit you can contact your insurance agent to adjust it.

The dwelling coverage limit may not cover the cost of rebuilding your house back to its pre-disaster state. Inflation and an increased labor demand can cause replacement costs to skyrocket following a natural catastrophe. Your policy limits are typically only updated once per year. You can increase your coverage limit if you know you'll need to rebuild your home in the future.

High arson and burglary rates in cities

Property crime refers to a wide range criminal acts, such as arson, motor vehicle theft, and larceny. While arson and burglary account for a large portion of property crimes, there are also many other types.

In 2020, Washington, DC had the highest property crime rate, with 3,493 crimes per 100,000 people. The city also had the highest violent crime rate, with 1,000 crimes per 100,000 residents -- more than twice the rate in Connecticut or Massachusetts. Maine had the lowest violent crime rate at just 8 percent.

Insurers offer discounts

You can receive many types of discounts when you purchase home insurance. Depending on the insurer, the discounts can be quite substantial. For example, State Farm provides a discount for customers who have been claim-free for five years. This discount can be incorporated into your policy's premium.

Some of the discounts that you can get when buying home insurance are cumulative, but not all of them. Insurers usually cap the savings at around 40%. However, not everyone is eligible for the maximum discounts. High-quality credit scores and clean records are typically eligible for the best discounts. Some insurers will also offer discounts for certain characteristics, such as zip code. You can also save money by only purchasing the insurance you need.

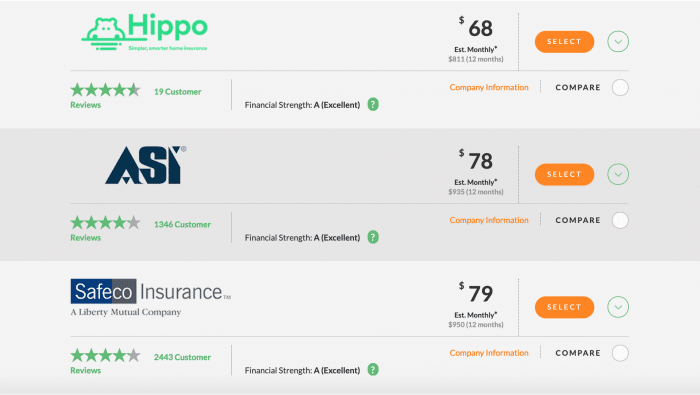

Choosing the cheapest provider

The best way to get home insurance at the lowest rate is to shop around for quotes. You can do this by visiting comparison websites. These websites let you enter some details about your home to compare different insurers. Some sites offer reviews on insurers. You should know how much your home will cost to replace in order to compare insurance companies. This will influence the rate you pay. This estimate should be done every few years.

Other than price, location is also important. Different insurers charge different premiums for different types of policies. However, a different insurer may offer lower premiums depending upon your location. For example, if you live in an area with high crime, you may not qualify for the same rates as someone who lives in a smaller town or city.